By: Phil Dawson

"GCs should be evaluating a new wave of 'affirmative AI insurance' offerings that provide targeted coverage for risks, such as hallucinations, bias, IP infringement and safety failures."

— Gartner Legal & Compliance Practice, April 2, 2026

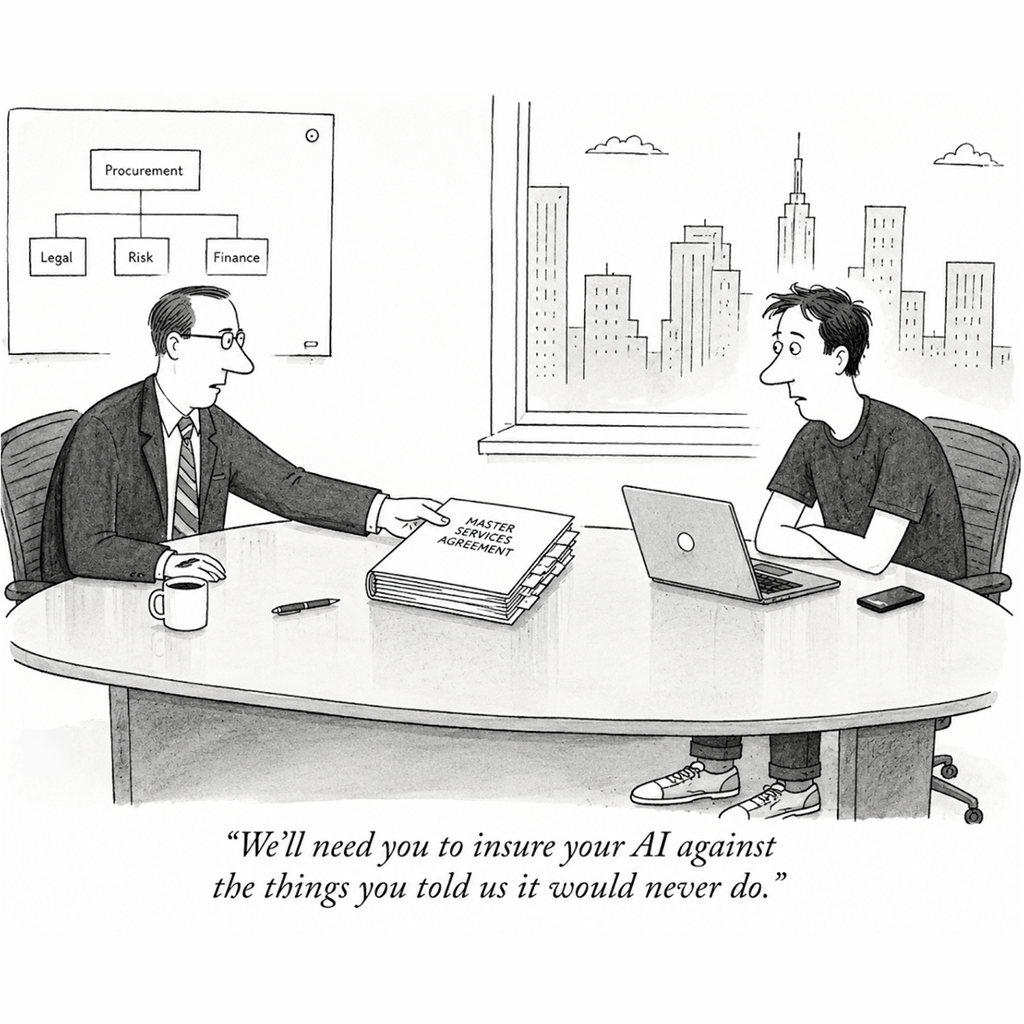

Large enterprises are now requiring their AI vendors to carry insurance for AI-related risks.

More specifically, Fortune 1000 companies are updating their MSAs and SLAs to introduce broad AI governance obligations, and the insurance requirements now extend beyond Cyber and Tech E&O to what is now simply called AI insurance. The clauses name AI-related risks and perils — AI bias and discrimination, copyright infringing model outputs, AI regulatory violations, and AI system failures or output harms — and require limits sized to the enterprise customer's exposure, often more than 10m per claim.

For mid-market AI providers selling into these accounts, AI insurance is moving from a specialty coverage discussion to a procurement requirement. In some cases, it is becoming a condition of doing business, even as AI insurance as a product category remains in its infancy.

So why are large companies getting ahead of traditional insurers on this? In short, AI as a strategic asset is too important to leave to uncertainty. In 2025, global corporate AI investment hit $581.7 billion, up 130% year-on-year (Stanford HAI, 2026 AI Index Report). AI litigation is rising in lockstep, and regulation is now operative, with AI legislation advancing across California, Colorado, Connecticut, New York, Virginia, and other states.

Against this backdrop, AI-related exclusions, sublimits, and coverage uncertainty are becoming more common across corporate insurance programs, raising questions about the reliability of silent coverage for AI-specific loss scenarios. AI is a core asset producing core liability, and the market is treating its risk transfer accordingly.

In the MSAs we have reviewed, the requirement for AI insurance typically reads along these lines:

"Provider shall obtain and maintain, at its own expense, insurance coverage for AI-related risks, including but not limited to coverage for claims of algorithmic bias and discrimination, hallucinations, copyright fringement, AI regulatory penalties, in amounts satisfactory to [Customer]."

— Vendor MSA from a Fortune 100 Company

In addition to the insurance requirement, three types of AI governance provisions are common across the agreements provided to us:

Procurement requirements for AI solutions are increasingly aligning with established third-party risk management practices, such as those used for cybersecurity. Armilla's underwriting reflects this same approach, reviewing the controls and assessments carried out by AI developers and deployers against these standard practices.

Three recent engagements at Armilla illustrate what this looks like in practice.

A decade ago, cyber risk sat unpriced inside traditional policies — "silent cyber" — until a wave of losses forced carriers to exclude it and build standalone products in its place. That transition took years. The same shift is now underway for AI, but on a compressed timeline. Multiple forces are converging at once:

Add the unprecedented speed of AI adoption, and the result is an environment of mutually reinforcing uncertainty around AI coverage that is picking up speed.

"This is highlighting a crucial blind spot for businesses. They are clamoring to join the AI bandwagon, but they have to pause and ask if they're fully protected."

— Ifeoma Ajunwa, Professor, Emory University School of Law, via Fast Company, May 2026

"More than 90% expressed interest in dedicated insurance cover for AI-related exposures, with two-thirds prepared to pay at least 10% higher premiums for such protection."

— The Geneva Association, October 2025

Armilla helps AI providers meet these requirements across three areas:

The changes we're seeing in AI vendor MSAs are recent. If you're finding them in your clients' contracts, review them against the current tower, identify where standalone AI coverage is warranted, and get in touch — we'd welcome the chance to share what we're seeing and explore where we can help.

Covering AI is Armilla's newsletter for insurance brokers and risk managers navigating the complexities of AI liability, risk management and governance.

Disclaimer: The insurance products described on this website are offered through surplus lines insurers. Surplus lines insurance is not subject to all the insurance laws and regulations of your state, and such insurers are generally not licensed by or subject to the supervision of the insurance department of your state. Coverage may not be available in all jurisdictions and is offered only through properly licensed surplus lines brokers.

Nothing on this website constitutes an offer to sell or a solicitation to buy insurance. No coverage will be bound or effective unless and until confirmed in writing by an authorized representative and all underwriting requirements have been satisfied. Any descriptions of coverage are for general informational purposes only and do not amend, modify, or supplement any actual policy or contract of insurance.

Please consult with a licensed surplus lines broker to determine availability and eligibility in your state.

Armilla Insurance Services is a Coverholder at Lloyd's. Affirmative AI Liability Insurance is underwritten by certain underwriters at Lloyd's. Not all activities are related to Lloyd's.